For most insurers, the claim defines the customer relationship. It is when a policy stops being a promise and becomes a payment, and for many carriers it is also the slowest and most expensive process they run, the one where operational improvement translates most directly into financial results.

AI claims processing automation is increasingly part of how leading carriers run the claims function. Applied across intake, document review, triage, fraud screening, and settlement of routine claims, it can shorten cycle times, reduce handling cost, improve the customer experience, and strengthen fraud defense. The question for most executives is no longer whether AI belongs in claims, but which use cases to prioritize and how quickly to scale them.

Key takeaways

AI claims automation helps insurers:

- •Reduce claims cycle times by up to 75 percent

- •Lower claims processing costs, often by 20 to 50 percent

- •Improve customer satisfaction with faster, clearer settlements

- •Strengthen fraud detection as AI-generated fraud rises

- •Increase adjuster productivity by an estimated 40 to 50 percent

Why claims is where time and cost accumulate

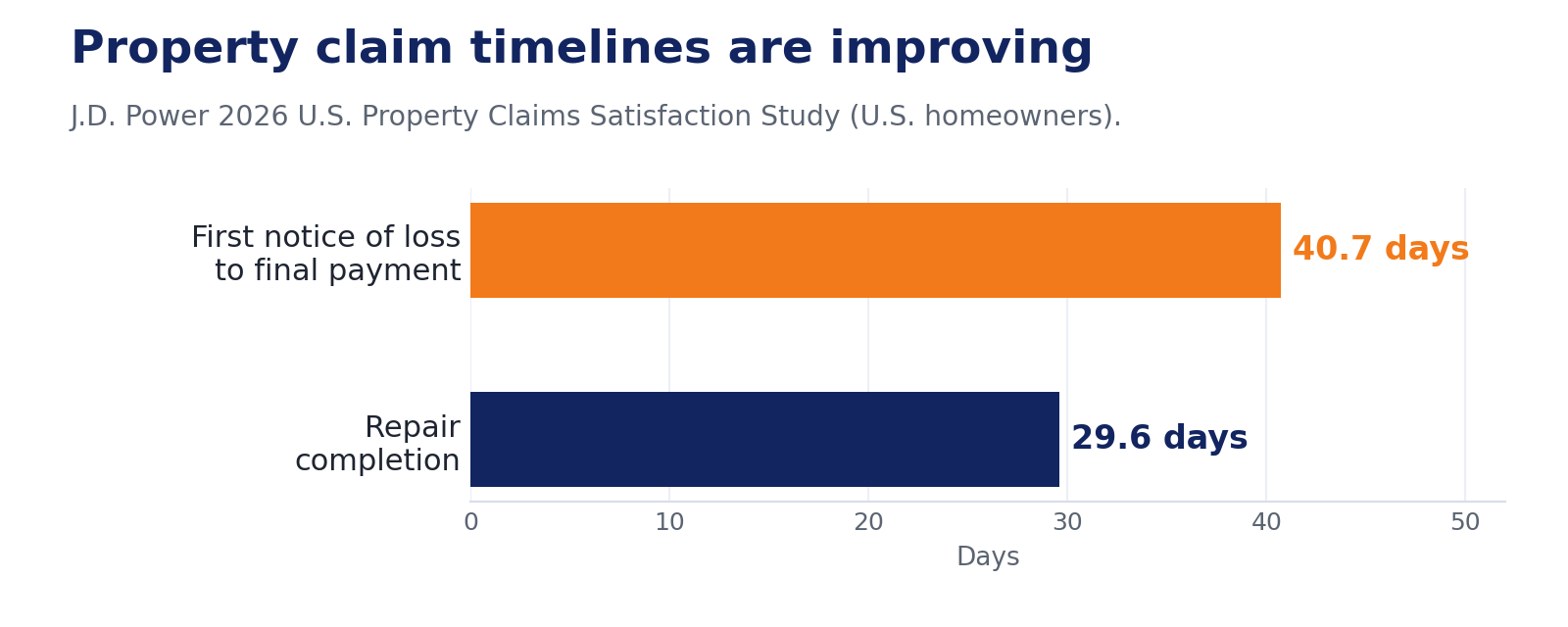

After several difficult years, the claims experience is improving, and technology is part of the reason. J.D. Power's 2026 U.S. Property Claims Satisfaction Study found that the average time from first notice of loss to final payment fell to 40.7 days, down 3.4 days year over year, while average repair time dropped to 29.6 days and overall satisfaction rose. J.D. Power credited investments in digital channels and the efficiency gains they enable.

Even after that progress, roughly 40 days from first notice of loss to final payment leaves real room to improve, and much of the remaining delay sits in administration rather than adjudication. Industry analyses attribute a large share of processing time to document handling rather than decision-making. Many carriers still run on legacy core systems spread across disconnected applications, so data does not flow cleanly, reserves can drift, and adjusters spend time rekeying information instead of resolving losses.

What AI claims automation actually does

Modern claims automation is not a single tool. It is a connected set of capabilities applied across the claim lifecycle:

- Intelligent FNOL intake. Conversational AI captures the first notice of loss and structures the data instantly, with no phone tree or PDF form.

- Document AI. Computer vision and language models read photos, estimates, and reports, then extract and validate the fields that matter.

- Triage and routing. Models score complexity, send simple claims to straight-through processing, and route the rest to the right adjuster with context attached.

- Automated adjudication. For low-value, low-risk claims that pass every check, the system can approve and pay in seconds, with human review held for where it adds value.

- Fraud and reserve intelligence. Anomaly detection flags suspicious patterns at intake, and predictive models keep reserves accurate as claims develop.

How AI cuts claims cycle time

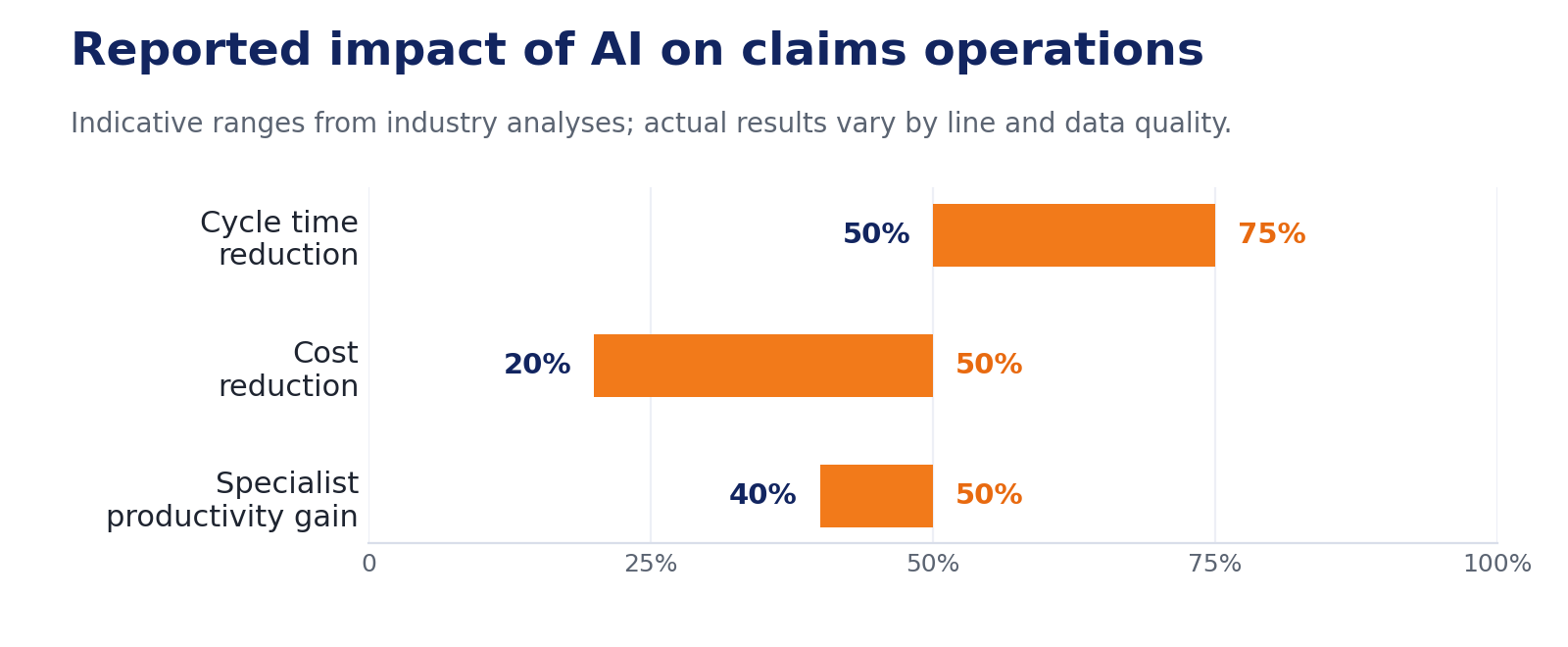

Cycle time is where the operational impact is easiest to measure. Reported results vary by line of business and data quality, but industry analyses commonly cite reductions of roughly 50 to 75 percent once AI handles routine claims, with a large share of simple claims processed straight through in minutes rather than weeks. Two carrier disclosures illustrate the range:

- Lemonade (an AI-native insurer) reports in its FY2025 annual filing that, as of year-end 2025, 96 percent of first notices of loss are taken by AI without human intervention and about 55 percent of claims are fully automated, with the simplest settled in as little as two seconds. These insurtech figures will not map directly onto a legacy book, but they show what a fully AI-native model looks like.

- Zurich has used natural language AI to read and summarize claims documents, reducing a review that previously took a claims handler hours or days to one completed in minutes.

In both cases the value follows the same pattern: automation absorbs high-volume, low-complexity work, freeing skilled adjusters for the claims that require judgment, investigation, or empathy.

How AI lowers claims processing cost

Shorter cycle times generally translate into lower unit costs. Published estimates vary, but analyses of AI in claims commonly put cost reductions in the 20 to 50 percent range for suitable claim types, driven by less manual effort per claim, higher straight-through processing, and the ability to absorb catastrophe and seasonal volume without adding headcount.

Productivity gains for claims specialists, often estimated at 40 to 50 percent, compound those savings, since the same team handles more volume without a drop in quality.

Aviva rewires motor claims with AI

Facing rising motor claims costs, the UK's largest general insurer rebuilt its claims journey with McKinsey's QuantumBlack team, deploying more than 80 AI models across the lifecycle. A "double helix" design lets each claim move between digital and human handling as needed. Reported results:

- •Liability assessment for complex cases: about 23 days faster

- •Claim routing accuracy: improved by roughly 30 percent

- •Customer complaints: down about 65 percent

- •Reported savings: more than £60 million in 2024 (per Aviva, via McKinsey)

Loss adjustment expense, the cost of investigating and settling claims, is one of the largest controllable line items in an insurer's combined ratio, so even a single-digit improvement flows straight to underwriting profit.

How AI improves the customer experience

In claims, speed and experience are closely linked. A policyholder who has suffered a loss mainly wants the claim handled quickly, clearly, and fairly, and automation can support all three.

When intake is conversational and decisions arrive in minutes, satisfaction tends to follow. Lemonade, for example, reports a net promoter score above 75 on its instant-claims product. More broadly, J.D. Power's research consistently links longer cycle times to lower satisfaction. The stronger programs keep people in the loop by design, routing sensitive matters such as personal injury to human handlers while automation manages routine claims.

How AI strengthens fraud detection

Fraud raises costs for every policyholder. The Coalition Against Insurance Fraud estimates it costs the United States $308.6 billion a year across all lines, a substantial portion of it in property and casualty, and a cost that ultimately feeds into premiums.

The threat is also changing shape. According to Gen Re, AI-enhanced insurance fraud cases in the U.S. jumped from fewer than 20,000 in 2022 to more than 80,000 in 2025, and Verisk found that 99 percent of insurers have encountered manipulated or AI-altered documentation. Rules-based systems built for a slower era are struggling to keep pace.

This is where detection capability matters most. Machine learning can identify patterns across claims, policies, and external data that static rules miss, while reducing the false positives that consume investigator time. Market analysis citing Coalition data puts the reduction in fraudulent claims from AI-driven detection at an estimated 10 to 30 percent, though results depend heavily on data quality and program design.

One caution worth stating plainly: detection is not investigation. A score tells you which claims to look at, not what happened. The most effective programs pair fast scoring with systems that read across sources, explain their reasoning in a way a regulator can audit, and route the right cases to skilled investigators.

The business case

Taken together, the operational gains add up to a measurable financial case.

The pattern holds at the enterprise level. McKinsey reports that a small cohort of insurance AI leaders generated 6.1 times the total shareholder return of laggards over a five-year period, a wider spread than in most other sectors. The same analysis notes that few insurers are yet extracting meaningful value from AI across the full value chain at scale, which means the opportunity for most carriers lies less in access to the technology than in disciplined, end-to-end execution.

For decision-makers, the relevant comparison is not only the cost of an AI program, but the cost of maintaining slow, manual claims handling while peers move faster.

A pragmatic path forward

In practice, the question for most carriers is not build versus buy in the abstract, but how to reach measurable results without a large fixed team and a long wait before the first return. Three principles tend to separate programs that deliver from those that stall: integrate AI into core claims systems rather than running isolated pilots, keep experienced people on complex claims, and design for regulatory scrutiny from the outset, so that every automated decision has an auditable basis.

Connexr works with insurers on this kind of phased implementation, designing claims AI around a carrier's existing systems, data, and compliance requirements and measuring it against defined targets such as cycle time, loss adjustment expense, and fraud leakage. As part of RSA Tech Group, its work is built for regulated environments, with SOC 2, HIPAA, ISO 27001, and GDPR compliance.

Find where AI fits in your claims operation

Connexr offers a focused readiness assessment that maps your highest-volume claim types, data, and systems to a phased plan with measurable targets such as cycle time, loss adjustment expense, and fraud leakage.

Frequently Asked Questions

Connexr is a division of RSA Tech Group | connexr.com | SOC 2 | HIPAA | ISO/IEC 27001:2022 | GDPR Compliant